Page 26 - Cover options

P. 26

INNOVATION

overall robust economic peaked in October 2018; power generation for 77.4%

growth. During Apr-Jan’19 nevertheless, moderated to of its electricity, while hydro

(FY19-YTD) period, power remain range bound constituted 10.3%,

demand rose 5.7% on a YoY between Rs 3.0-3.6/unit renewables 9.3%, and rest

basis driven by traction in since November 2018. from other sources.

West, South and However, the share of

On the supply side,

East regions. renewables is slowly inching

generation growth has kept

On backdrop of strong power pace with demand growth at up with increasing capacity

additions in this segment.

demand growth, the 5.8% in FY19-YTD on a YoY

merchant market basis. India relies on thermal

environment has also been

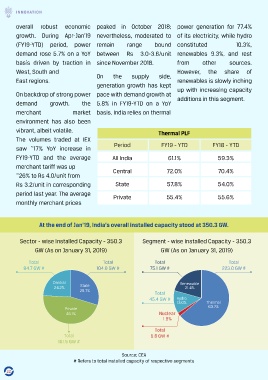

vibrant, albeit volatile. Thermal PLF

The volumes traded at IEX

Period FY19 - YTD FY18 - YTD

saw ~17% YoY increase in

FY19-YTD and the average All India 61.1% 59.3%

merchant tariff was up

Central 72.0% 70.4%

~26% to Rs 4.0/unit from

Rs 3.2/unit in corresponding State 57.8% 54.0%

period last year. The average Private 55.4% 55.6%

monthly merchant prices

At the end of Jan’19, India’s overall installed capacity stood at 350.3 GW.

Sector - wise Installed Capacity - 350.3 Segment - wise Installed Capacity - 350.3

GW (As on January 31, 2019) GW (As on January 31, 2019)

Total Total Total Total

84.7 GW # 104.0 GW # 75.1 GW # 223.0 GW #

Central Renewable

24.2% State 21.4%

29.7%

Total

45.4 GW # Hydro

13.0% Thermal

Private 63.7%

46.1% Nuclear

1.9%

Total

Total 6.8 GW #

161.5 GW #

Source; CEA

# Refers to total installed capacity of respective segments

22